By Wagemann + Partner PartG mbB, Berlin, Dr. Filip Schade, Steuerberater, Master of Laws

Edited By Integra International Grant Gilmour, CPA (Canada, BC) CPA (USA, Arizona)

Question: Is there an internationally coordinated set of rules regarding the legal and tax treatment of private foundations and trusts?

Answer: The OECD has hardly any recommendations available and there are no harmonization efforts observable. Private foundations and trusts remain a purely national and sometimes regional matter.

When preparing this article, I asked myself whether there is an international set of rules in which many countries have agreed on certain principles for the legal and tax treatment of private foundations and trusts. After all, we live in a globalized world. Private foundations and trusts, unlike, for example, cryptocurrencies and blockchain, are nothing brand-new. Since the OECD has published a Model Tax Convention on which many tax treaties around the world are based, I assumed that the OECD had already dealt with private foundations and trusts and that corresponding recommendations could be found in the Commentary on the OECD Model Tax Convention .

To my surprise the OECD hardly makes any recommendations about private foundations and trusts in terms of their tax treatment in an international context. The only statement that can be found in the Commentary on the OECD Model Tax Convention is simply that a private foundation or trust can be a person entitled to the benefits of a Double Tax Treaty if its State of Founding grants it legal personality and if it is thereby subject to Corporate or Personal Income Tax in this State. However, one searches in vain in the Commentary on the OECD Model Tax Convention for how distributions by a private foundation or trust to its beneficiary are to be classified under Tax Treaty Law from the OECD’s point of view. Even the terminology around the world is not consistent. In some countries we use the words Foundation and others the words trust. In some countries these words are exclusive to charities and in others they are exclusive to private enterprises. Confusion is the result.

What is there to report about the European Union? Due to the ever-increasing popularity of foundations, there was a proposal from the EU Commission to introduce an EU-wide legal form for foundations in 2012. However, this proposal envisaged the creation of an EU-wide uniform legal form for the pursuit of charity purposes. Ultimately, the proposal failed in 2015 due to manifold criticism from the EU Member States. It is surprising that the harmonization of the law on private foundations of the EU Member States as well as the agreement on a uniform tax treatment of private foundations within the EU was never seriously considered. Therefore, it can be stated that we can hardly speak of internationalization of foundation law. Foundation law as well as the requirements regarding the taxation of private foundations or trusts and their founders and beneficiaries remain a purely national area of law. The effect is that there is still a hotchpotch of various unilateral requirements regarding the establishment of private foundations or trust, of their organization or the achievement of the foundation’s purpose. This legal disorganization can be clearly seen, for example, in the different names for private foundations in their respective States of Founding.

Why is it then important to understand private foundations or trusts in an international context? There are two main reasons for this: Firstly, since there are no uniform international regulations, it is important to develop a basic understanding of the subject in order to avoid misunderstandings resulting from differences in national legislation. Writing this article serves the purpose of exchange of professional experience and knowledge. This is particularly important because my colleagues in Integra have made experience that there are often problems of understanding when it comes to the topic of private foundations and trusts. For continental Europeans, for example, it is difficult to understand why the trust is so popular in the U.S. and why anyone can set it up in a short time without having a certain amount of starting capital. In comparison, in Germany and probably in other countries as well, the process of setting up a private foundation is much more formalized. In Germany, for example, no private foundation can be established without sufficient time and a certain amount of starting capital. In addition, I would like to point out that the establishment of a German private foundation must be carefully considered by the founder. For example, once a German private foundation is set up, the one-way principle must be observed. The property given to the private foundation can only be retransferred to the founder in very exceptional cases. The same applies to changes in the foundation’s deed. Finally, a private foundation in Germany counts as a legal entity and can therefore be bearer of rights and obligations. These are all significant differences compared to a U.S. trust. Accordingly, the purpose of this article is to open up the conversation as it is so important in order to clear up existing misunderstandings and make your everyday practice easier.

Potential consequences of different conceptual understandings in each country.

- Different conditions of domestic laws regarding approval of foreign private foundations and trusts

- Possible differences in the tax treatment of private foundations, their founders and the beneficiaries in cross-border situations in the area of income tax and inheritance/gift tax

- Significance for practice: tax advantages, but also risks in cross-border situations

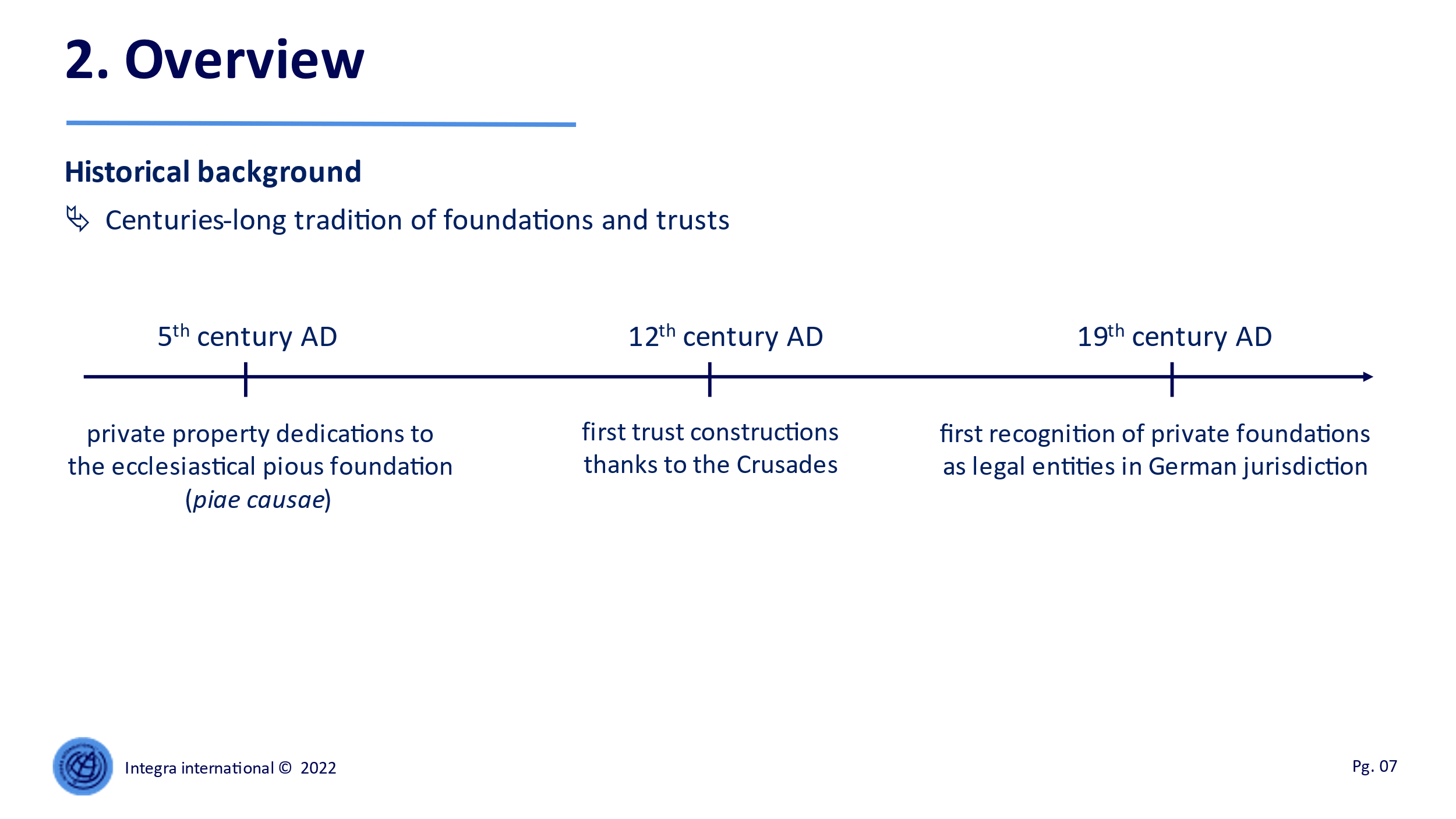

The second reason is the consequence of the continuing unilateralism in the area of foundation law and the tax treatment of private foundations and trusts. This can have advantages and disadvantages, especially in terms of taxation. The different conditions regarding the domestic recognition of foreign foundations and trusts and the related divergences regarding the tax treatment of private foundations, founders and beneficiaries in cross-border cases may lead to mismatches, possibly resulting in a non-taxation of the distributions of the private foundation to the beneficiaries. Then again, the mentioned mismatches can also lead to multidimensional double taxation: on the one hand with income tax in two different countries or with income and gift or inheritance tax in one and the same country. Such cases are not uncommon in German advisory practice, as we are increasingly confronted with enquiries from clients who are tax residents in Germany regarding tax implications of U.S. trusts and private foundations, particularly in Liechtenstein or Switzerland. The existing unilateralism in the area of foundation law and the tax treatment of foundations and trusts is actually surprising. When I prepared this article and researched the topic of private foundations and trusts, I found that foundations and trusts are not inventions of the 19th century, but rather historically anchored.

Hence, they have a centuries-long tradition and are globally widespread legal forms. Foundations created by individuals have been appearing since around the 5th century AD, initially in the form of the so-called pious foundation. Such a foundation was established for – generally speaking – ecclesiastical and social matters. In this case, the foundation was not a private subject with legal personality, but special property of the church. The private founder transferred property to the church, which the church administered in trust for pious purposes. The feudal origins of a trust can be traced to the 12th century in England. The fiduciary construction of the trust owes its origin to the Crusades. The basic idea was based on economic considerations, as the feudal landowner participating in a crusade needed a suitable and reliable administrator of the property during his absence. This person had to have sufficient managerial power and competencies. These were regulated in a “set” of legal relationships. Within these legal – more precisely – trust relationships, the feudal landowner transferred his property to the administrator – namely the trustee – with the binding condition that this property would be transferred back to him upon his return. Thus, the previous owner of the property participating in the crusade became the beneficiary under the agreement. Typically, persons from the feudal landowner’s circle of acquaintances and friends may have been preferred as trustees. However, the pious foundation as well as the 12th century trust construct were not independent entities with legal capacity. Besides, these constructs were either about donations of property to the church or for other charitable purposes, or about asset management for a limited period of time. Private foundations that could be established for an indefinite period were first recognized as independent legal persons in the German jurisdiction in the 19th century. Moreover, at that time the foundation could not only be established for charitable purposes, but was increasingly accepted as a legal form for the permanent commitment and administration of a founder’s property. This paved the way for private foundations in Germany. Well-known German foundations are, for example, the Adidas Foundation, the Daimler and Benz Foundation or the Siemens Foundation.

Term and delimitation of a private foundation or trust

- A foundation is an entity which is endowed by a founder with certain property, and which uses this property to permanently realize the purpose of the foundation as determined by the founder.

- Note: no association or company-like organization of the foundation, i.e. no members or shareholders

- Need for distinction between foundations without legal capacity and foundations with legal capacity

- Need for distinction between charitable and private family foundations based on the purpose of the foundation

What exactly are private foundations? What do they mean and how can they be distinguished from other types of foundations? In general, a private foundation is understood to be an entity that is endowed with certain property by a founder, and which uses this property to permanently realize the purpose of the foundation determined by the founder. In this context, I want to emphasize that foundations do not have an association- or company-like organization, that means a foundation has – unlike an association or a company – neither owners nor members or shareholders. However, the foundation can benefit a certain group of persons. The foundation property is managed by a person or group of persons appointed in the foundation deed. Apart from this, a distinction must be made between foundations without legal capacity and foundations with legal capacity, as it is the case in the German legal system. The foundation without legal capacity are not legal entities. They are established by transferring property to individual or other legal entities – these usually act as trustees. A foundation with no legal capacity is also referred to as a fiduciary foundation. From a civil law perspective, the trustee, that means the foundation holder, is the legal owner of the foundation’s property and becomes the bearer of rights and obligations. In contrast, the foundation property can be accounted to either the founder or the trustee from a tax perspective. Foundations with legal capacity have their own legal personality and, consequently, are legal entities. However, they cannot be classified as companies, since – as already mentioned – they have no members or shareholders. Furthermore, the purpose to be pursued by the foundation or trust may vary. In this context, the distinction between charitable and private foundation is particularly relevant. Thus, charitable foundations realize certain purposes serving the common good. From a German perspective, such purposes include the promotion of science and research, art and culture, or nature conservation. In Germany, for example, these foundations enjoy far-reaching tax benefits. Private foundations, on the other hand, serve exclusively the interest of one or more families. This is why such foundations are also called family foundations in Germany. Accordingly, the beneficiaries are members of the family.

Selection of motives of the establishment of a private foundation or trust

- Instrument of succession planning => securing and preserving the founder’s legacy

- Long-term preservation of company and private wealth => separation of business and private property

- Asset protection and asset management

For what reasons are foundations established? This is obvious in the case of charitable foundations. In the case of private foundations or trusts, various reasons play a role. The establishment of a private foundation or trust can be primarily aimed at succession planning. Accordingly, the establishment of a private foundation is intended to preserve the continuity of the company and to prevent the sale of the company. It is, therefore, about securing and preserving the founder’s lifetime achievement or legacy. In addition, descendants who are not eligible for the family-internal continuation of the company can be excluded from the future management of the company. The company can be continued by third parties, which also allows the company’s goals to be pursued beyond the founder’s death. In this context, the foundation offers the possibility of keeping business and private property separated from each other. Particularly in constellations in which, on the one hand, a family business is to be permanently preserved and should remain independent, and on the other hand, descendants are not necessarily considered as entrepreneurial successors, a private foundation helps to secure both the business and the descendants economically in the long term. That is why German scholars also speak of the protection of property from the family for the family.

What does that mean exactly? In this context, imagine the following scenario. Your client is a successful entrepreneur – he develops and sells highly complex software in medical technology. However, he is single and childless. The only heir is his sister. She has nothing to do with medicine or software development, because she is a cashier for a food retailer. So, the client does not want his sister to take over the management of his business after his death. He is worried that management and software development will overwhelm her, so that his entrepreneurial legacy will not be continued after his death. Instead, he would prefer to instate his experienced employees as company managers. In Germany, for example, this can be achieved by setting up a private foundation.

Another example: A wealthy couple has a son who is unable to work and run a household due to his disability. He is therefore in need of care and dependent on the financial help of his aging parents. After the parent’s death, a legal guardian would decide on the son’s finances in Germany. In order to prevent a unsuitable person from being nominated as the son’s guardian and not taking care of the son’s needs appropriately, the establishment of a private foundation can be recommended in such situations in Germany. The parent’s property can then be transferred to the private foundation and the management of the foundation’s property can be entrusted to persons whom the couple chooses independently and whom they consider competent and trustworthy. In addition, the managers of the foundation’s property – this is in Germany the management board – are bound by the founder’s will, which is recorded in the foundation deed. Consequently, a child in need of care can be financially secured after the death of the parents and the necessary medical care can be guaranteed to an extent determined by the parents.

Moreover, the private foundation offers the possibility of asset protection and asset management. Asset protection aims to protect family or company property from the founder’s creditors or from being split in the event of a divorce or a dispute between heirs. Asset management is not only about protection and preservation of property, but also about investing. Accordingly, the goal is asset protection and return-oriented and risk-diversified asset growth.

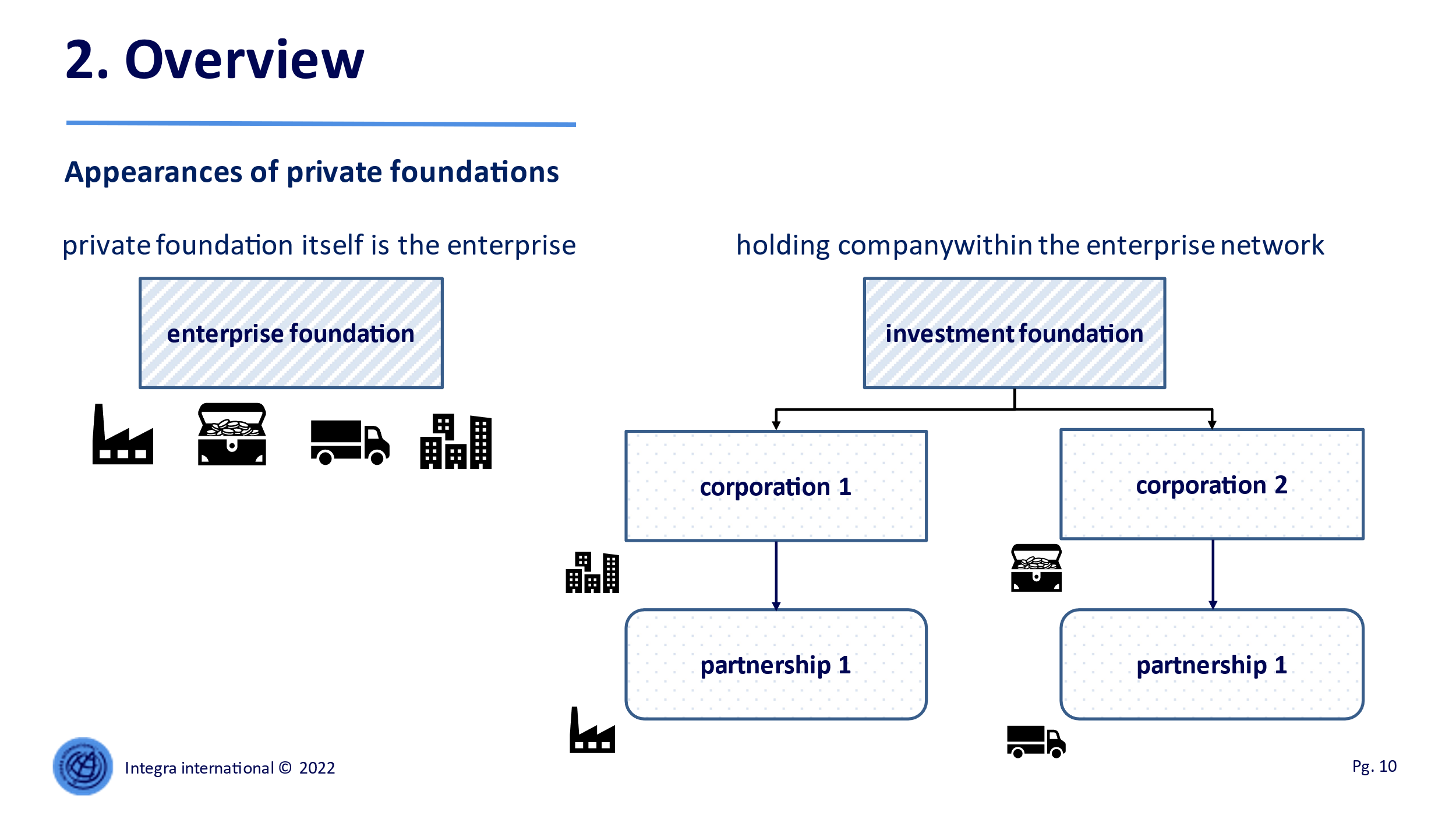

Appearances of private foundations

After having looked at selected reasons for setting up a private foundation or trust, the next question is what forms private foundations can have. In Germany, a distinction is made between two main forms of business-related private foundations: These are the so-called enterprise foundation and investment foundation. In the case of the enterprise foundation, this foundation itself manages the business. The foundation’s managers are directly responsible for the management of the business. In German practice, enterprise foundations often prove to be relatively unsuitable because the necessary flexibility of the company to adapt to future market situations – for example the current energy crisis – and the associated need for restructuring measures is not guaranteed. This required flexibility is instead given in the case of investment foundations. A private foundation is referred to as an investment foundation if it acts as a holding company and is a member or shareholder in one or more subsidiaries that carry out the business.

In the example above, these are the corporations and partnerships with various functions within the enterprise network. From a German perspective, such foundations are suitable on the one hand for succession planning and on the other hand for the long-term preservation of the company.

This is how the foundation and trust system works in Germany. Let’s start the discussion of how it is similar and different in each of our Integra members countries. Understanding what is similar and what is different will help us all eliminate confusion and advise our clients.

References:

- Kraft, Gerhard: Die Familienstiftung als Erkenntnisobjekt der Betriebswirtschaftslehre, in: Anwendungsorientierte steuerliche Betriebswirtschaftslehre – Festschrift zum 65. Geburtstag von Heinz Kußmaul, Erich Schmidt Verlag 2022, p. 605-616.

- Kraft, Gerhard: Ungeklärte Problembereiche der Besteuerungssystematik ausländischer Familienstiftungen unter besonderer Berücksichtigung von Trust-Konstruktionen des anglo-amerikanischen Rechtskreises, in: Globalisiertes Steuerrecht – Festschrift für Heinz-Klaus Kroppen, Verlag Dr. Otto Schmidt 2020, p. 631-645.

- Kutac, Kimberly: Die Familienstiftung in Deutschland und Liechtenstein, Internationales Steuerrecht 2021, p. 409-418.

- Schienke-Ohletz, Tanja / Kühn, Michal F.: Doppelbesteuerung bei Auskehrungen aus ausländischen Trusts?, Deutsches Steuerrecht 2022, p. 1413-1416.

- Stöber, Michael: Die geplante Europäische Stiftung, Deutsches Steuerrecht 2012, p. 804-808.

- Weitemeyer, Birgit: Kommentar zu § 80 BGB, in: Münchener Kommentar zum BGB, Verlag C.H.Beck, 9th edition 2021.

About The Author

Dr. Filip Schade, StB, LLM

Tax Advisor

![]()

Filip Schade qualified as German Tax Advisor in 2021. Before joining Wagemann + Partner PartG mbB as an international tax specialist in 2022, he did his PhD in European and International Tax Law at a German university. He has his master degree in German and Polish Law.

Filip offers tax consulting services primarily to foreign as well as to German companies and individuals regarding international cases.

Filip gives also lectures in German and International Tax Law at two German universities and has written numerous articles on taxation published in German and foreign tax journals.